To download the PDF copy, click here: Lighthouse Wealth Management Outlook: April 2026

Market Outlook

In an August 20, 2011, essay published in The Wall Street Journal, venture capitalist Marc Andreessen famously argued that “software is eating the world.” His theory: “We are in the middle of a dramatic and broad technological and economic shift in which software companies are poised to take over large swathes of the economy.” From Silicon Valley’s dislodging of Hollywood in entertainment dominance, to the key role of software-powered drones in warfare, his vision has proven eerily accurate in hindsight.

A decade later, artificial intelligence (AI) was providing software developers with significant productivity gains in basic, repetitive and time-consuming tasks. To the extent that AI could write software, this automation enabled developers to allocate more of their time to the most difficult aspects of their jobs.

Early this year, the narrative suddenly changed. With recent releases of Anthropic’s Claude Cowork tool and OpenAI’s enterprise agent, Frontier, investors suddenly began to perceive AI not just as a tool for humans writing software, but as a potential replacement for software itself. That is, “Software may have eaten the world, but AI is about to eat software.” In mere weeks, the perceived risks of Software as a Service (SaaS) companies’ business models have jumped as their share prices have cratered.

Source: YCharts Retrieved 4/14/2026

The “SaaS apocalypse” fears also weighed heavily on the software lending market. As the chart below depicts, yields on loans to software companies have spiked in recent weeks. Default fears on such loans held by private credit funds (often totaling 20–30% of their assets) have precipitated a record level of redemption requests, forcing the funds to “gate” their liquidity.

Source: Apollo Chief Economist

No one doubts that AI will have a material impact on nearly every facet of the economy over the next decade. But to paraphrase Mark Twain, it seems to us that “the reports of software’s death are greatly exaggerated.”

We would draw a meaningful distinction between AI’s capacity to change how software is written (and/or functions) and its capacity to make software unnecessary altogether. For many businesses, software applications are mission-critical and not easily replaced by AI. Admittedly, vendors with low switching costs and weak enterprise integration may be facing existential risk. But for vertical- or domain-specific SaaS vendors addressing complex industries and/or controlling unique proprietary data, the AI revolution may ultimately impel them to higher growth as AI agents are integrated into incumbent systems.

It is certainly possible that Claude AI (or a similar system) could become so advanced that nearly every company decides to use it to replace all their existing software vendors over the next several years. As far as non-listed companies are concerned, Golub Capital recently reported that “mission-critical enterprise software businesses” in its Golub Capital Altman Index (GCAI) grew earnings by 4% year-over-year in Q1 2026 compared to Q1 2025. We will keep a close eye on earnings releases of publicly listed software companies to see how much of their top and bottom lines are actually being consumed by AI.

Financial Market Review

The S&P 500 Index lost 4.4% in the first quarter, as declines in large-cap growth stocks (9.8%) more than offset 2.0% gains in large-cap value stocks. Mid- and small-cap stocks showed a similar pattern: mid-cap growth fell 6.4% while small-cap growth declined 2.8%, whereas mid-cap value rose 3.6% and small-cap value gained 4.9%. International indexes were up for the quarter (1–4%), despite the U.S. dollar’s slight gain against most major currencies.

U.S. stock sectors exhibited tremendous dispersion in the quarter. Energy shares rose nearly 38%, with two-thirds of that runup occurring before the U.S. initiated military operations in Iran. Materials shares gained 10.7%. Financials, Consumer Discretionary and Technology sectors posted the largest losses (9.4%, 8.6% and 7.6%, respectively). Every Magnificent Seven stock posted a decline, as fears of AI replacing subscription software and doubts about returns on heavy AI investment spending weighed on share prices. Microsoft was the Seven’s biggest loser, down 23.2%.

The Bloomberg Commodity Index rose 23.3% as the price of crude oil spiked nearly 80% in the quarter. Precious metals continued their record 2025 run into 2026 (silver was up over 60% YTD in January), before turning sharply downward after news that Kevin Warsh would become the next Federal Reserve chairman. (Investors appeared to interpret Warsh’s nomination as reinforcing the Fed’s anti-inflation credibility.) Despite the correction, gold and silver still managed to finish Q1 up nearly 9% and 6%, respectively.

A modest rise in yields weighed on bond prices as the Barclays Aggregate Index generated a flat return. Intermediate-term municipal bonds were down 0.4%, with investment-grade and junk-rated corporate bonds down by similar amounts. “Real yields” on inflation-protected securities held firm, enabling TIPS to post returns in the 0.5%–1.0% range.

In addition to [temporary] inflationary pressures due to rising energy prices, we continue to see structural reasons as to why intermediate-term interest rates may remain higher for longer:

- American yields are competing against rising yields in other G7 bond markets.

- Federal deficit spending and borrowing are only likely to increase.

- Increasing corporate bond issuance from AI/cloud computing “hyperscalers.”

Economic Conditions

GDP rose at a seasonally and inflation-adjusted annual rate of just 0.5% in the fourth quarter, hampered by a record-long government shutdown that saw government spending tumble. For the full year, GDP posted a 2.1% increase. In 2024, the economy rose at a 2.8% pace. The Atlanta Fed’s GDPNow model forecast for Q1 real GDP growth is 1.3%.

The Consumer Price Index (CPI) rose 3.3% year-over-year in March, with nearly three-quarters of the monthly spike driven by rising gasoline prices. Core CPI, which excludes food and energy costs, came in at 2.6%. February’s Core PCE (the Fed’s key metric) was up 3.0% year-over-year, versus 3.1% in January. The University of Michigan’s index of consumer sentiment tumbled to the lowest-recorded level in its 70-year history as fears mounted over rising energy prices and the broader impact of the Iran war.

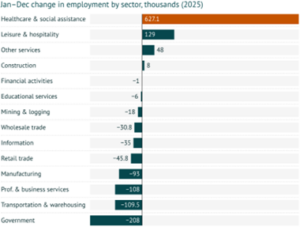

Nonfarm payrolls rose to a seasonally adjusted 178,000 in March, a reversal from the 133,000 decline in February. Health care was responsible for more than 40% of the growth. The unemployment rate edged lower to 4.3%, largely from a sharp reduction in the labor force (369,000). The share of working-age Americans in the labor force fell to 61.9%, the lowest since November 2021. Wages rose less than expected, with average hourly earnings up 3.5% from a year ago.

Source: Bureau of Labor Statistics

After cutting its key short-term rate three times in 2025, the Fed left its target range unchanged at 3.50%–3.75% in March. The Fed’s “dot plot” median projection is for only one 0.25% rate cut for the rest of 2026. The futures market is currently pricing a 40% chance of at least one rate cut later this year.

The Fed raised its 2026 core PCE inflation forecast to 2.7% (up from 2.5% in December). Chairman Jay Powell highlighted that a “big chunk” of core inflation is currently attributable to the lag effects of tariffs on goods. If confirmed by the Senate, Kevin Warsh would take over as chair when Powell’s term expires in May. Given Trump’s history of complaints about excessively high interest rates, his nomination of an “inflation hawk” like Warsh was an unexpected one.

The youngest person ever appointed to the Federal Reserve Board, Warsh was a central figure during the Global Financial Crisis, serving as then-Chairman Ben Bernanke’s primary liaison to Wall Street. He established his “hawkish bona fides” as he expressed skepticism toward the Fed’s protracted easy-money policy in the wake of that episode, as well as during the post-Covid inflation surge.

Asset Class and Sector Survey

Prior to the Iran war’s inception, a significant amount of the world’s essential commodities passed through the Strait of Hormuz, including 20% of global oil transits, 20% of seaborne liquefied natural gas, 30% of seaborne fertilizer, 40% of sulfur and 25–30% of the world’s helium supply. In addition to the obvious impacts of higher fuel costs for personal vehicles, commercial trucks and airplanes, a prolonged crisis in the Strait would disrupt the pricing and logistics of countless goods and services all over the globe.

Source: Trading Economics. Retrieved 4/14/26

Consumer goods packaged in plastic, as well as fabrics used in clothing, are derived from petroleum. Helium is essential for MRI machines and semiconductor manufacture. Sulfuric acid is required in copper production. The U.S. obtains 51% of its nitrogen fertilizer from the Persian Gulf; a disruption in that flow would cause a material spike in food prices.

After losing 9% for the year through March 30th, the Nasdaq has posted consecutive gains for 12 subsequent trading sessions and is now up 5.7% YTD on optimism that the Iran conflict has [largely] been resolved. Whether or not the Strait of Hormuz remains “fully open” as advertised is anyone’s guess, but stock prices do not seem to reflect much downside risk.

The forward price-to-earnings ratio on the S&P 500 currently stands at 20.9x. While that figure is down from 22.0x on December 31st (due to earnings growth estimates exceeding stock price increases), it remains well on the higher side of the Index’s historical valuation range. FactSet currently estimates Q1 year-over-year earnings growth at a robust 12.6%. Should the ceasefire break and the Strait’s maritime traffic become constricted for a period of months, those estimates would certainly be materially revised downward as a recession unfolded. As political and economic circumstances stand today, we remain neutral in risk allocations.

Please reach out to us if you would like to discuss capital markets or your personal financial plan.

Teancum D. Light, JD, CPA, CFP®

President

Chief Investment Officer

Disclosures: This material is for informational purposes only and is not rendering or offering to render personalized investment advice or financial planning. This is neither a solicitation nor a recommendation to purchase or sell an investment and should not be relied upon as such. Before taking any action, you should always seek the assistance of a professional who knows your particular situation for advice on taxes, your investments, the law or any other matters that affect you or your business. Although Lighthouse Wealth Management has made every reasonable effort to ensure that the information provided is accurate, Lighthouse Wealth Management makes no warranties, expressed or implied, on the information provided. The reader assumes all responsibility for the use of such information.