Download a PDF copy of the Lighthouse Wealth Management: Outlook – July 2024

Just weeks after salvaging the bulk of its army from the beaches of Dunkirk in June of 1940, Britain soon found itself again in dire straits. The German Luftwaffe launched a campaign to gain control of British airspace. Initial attacks on planes were followed by assaults on airfields and infrastructure. As the battle progressed throughout the summer, even civilians were deliberately targeted in terror bombing raids.

On August 20, 1940, Prime Minister Winston Churchill succinctly summarized the gratitude of every Briton to its airmen (as well as pilots from other countries): “Never in the field of human conflict was so much owed by so many to so few.”

Decades later, it remains difficult to argue against his math. Roughly 3,000 Royal Air Force and Royal Navy pilots defended 40 million inhabitants—and Western civilization—from a military juggernaut that had previously proven unstoppable. The Battle of Britain truly was a case of a tiny minority protecting the overwhelming majority.

While the stakes are immeasurably lower, we’re at a loss to find a better quote than Churchill’s to describe the stock market these days. The S&P 500 is up 15% so far this year. A single stock—NVIDIA—accounts for almost a third of that figure. Another four stocks—Microsoft, Amazon, Meta and Eli Lilly—collectively bring the total up to 55%. The top 10 stocks in the S&P 500 now comprise a record-high 38% of the S&P 500 Index.

Source: JPMorgan.

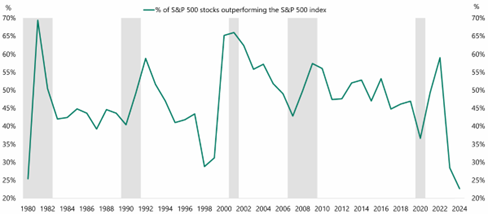

Conversely, there has not been a period in contemporary market history when so many individual stocks within the S&P 500 have failed to match the performance of the Index. Trillions in newly minted wealth has come down to just a handful of companies.

Source: Apollo Chief Economist.

Financial Market Review

The S&P 500 rallied for the third consecutive quarter, returning 4.4% through June 30. All the “Magnificent Seven” stocks posted positive returns; NVIDIA jumped nearly 37%, with Apple and Google up 23% and 21%, respectively.

Along with technology (8.8%) and communications services (5.2%), utilities were also positive for the quarter (4.6%). Expectations for massive electricity requirements as artificial intelligence (AI) rolls out have made power company stocks a beneficiary of the AI revolution. All other sectors were down, barring consumer staples (1%).

Large-cap growth was the only U.S. “style box” with a positive return in Q2. Large-cap value shares were off 2.1%; all mid- and small-cap sectors were down 3% or more. Developed international stocks were flat during the quarter. Emerging market indexes were up 4% to 5%.

Expectations of higher-for-longer interest rates have boosted the U.S. dollar against all major currencies in 2024. The dollar’s gains reflect America’s relative economic strength versus the rest of the world, as well as interest rates above those of its peers. The Swiss franc and Japanese yen have lost the most versus the U.S. dollar (USD), down 5.7% and 11.8%, respectively, year to date. The yen reached its lowest level since April 1990, breaking ¥160/USD. In late May, Japan confirmed its first currency intervention since 2022 in an effort to prevent the yen from slipping further.

Geopolitical tensions and increased central bank purchases boosted gold prices during the quarter. Yellow metal was up over 5%, while silver rose more than 16%. The Bloomberg’s Commodity Index rose 1.5% in Q2, as crude oil prices fell slightly.

The Bloomberg Aggregate Bond Index returned 0.07%. Intermediate-term Treasury yields climbed considerably in April, before dropping back close to their March 31 levels. The anemic performance of Treasurys was offset by positive returns for mortgage and corporate bonds.

Economic Conditions

Real GDP grew at a 1.6% annualized rate in Q1, well below the 2.4% survey estimate and far off the 3.4% gain in Q4 2023. Falling employment levels have underscored the slowing economic growth; June’s unemployment rate rose to 4.1% as April and May payroll gains trended downward by 111,000. Other indicators of labor market weakness: a higher percentage of Americans remain unemployed long-term and a reduction in hiring temporary workers.

Inflation is finally showing signs of slowing in earnest. For the first time since May 2020, the Consumer Price Index (CPI) declined month-over-month in June (0.1%). The annualized rate of inflation is 3.0%. Core CPI, which excludes food and energy prices, was 3.3% yearly, its lowest rise since April 2021.

After keeping short-term interest rates at a two-decade high for over a year, the softening inflation readings have reached a level where Federal Reserve Chairman Jay Powell has begun to signal that a change of course may be pending. “For a long time, the risks were more that we would fail to hit our inflation target,” Powell testified to Congress last week. He noted that “the labor market has cooled really significantly across so many measures,” and that “we’re very much aware that we have two-sided risks now.”

Powell clarified that he would not wait for inflation to reach the Fed’s 2% target before commencing the rate cutting. “You don’t want to wait until inflation gets all the way down to 2%. If you waited that long, you probably waited too long, because inflation will be moving downward and would go well below 2%, which we don’t want.”

The CME Group’s FedWatch tool now puts roughly 92% odds on at least one interest rate cut by the Fed’s policy meeting concluding September 18 and a 90% chance of 0.50% or more reductions before New Year’s Day.

In previous newsletters, Lighthouse Wealth has commented on the “inverted yield curve” as a reliable recession indicator., i.e., when 2-year Treasury notes yield more than 10-year Treasury notes, a recession usually occurs within 12 to 18 months. As with much else in this post-COVID era, a new record has been set. After 24 months of inversion, a recession has yet to transpire.

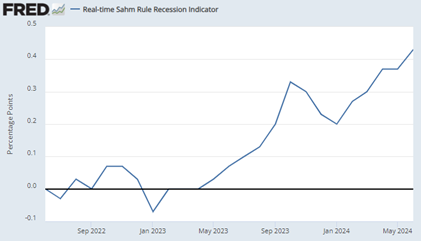

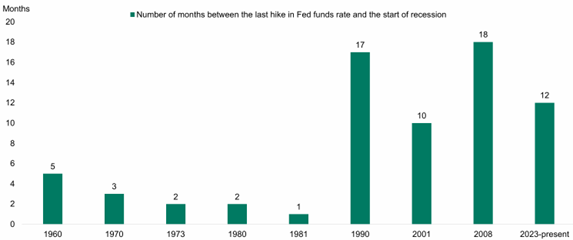

Two other recession indicators are worth pointing out:

- “The Sahm Rule” indicates that the early stage of a recession is signaled when the three-month moving average of the U.S. unemployment rate is 0.50% above the lowest three-month moving average unemployment rate over the previous 12 months. The Rule has successfully predicted the prior nine U.S. recessions back to 1970. As of June, the indicator stood at 0.43%—just below the critical level.

Source: Federal Reserve Bank of St. Louis

- A recession typically unfolds within 18 months after the Fed stops raising rates. We’re currently in month 12.

Source: Apollo Chief Economist

Numerous signs of stress are appearing amongst lower-income households. Corporate earnings calls are citing more cost-conscious consumers. The Federal Reserve Bank of New York reported that the percentage of credit card balances that fell into delinquency rose to nearly 9% last quarter—the highest in over a decade. Nearly 8% of drivers were at least 30 days behind on their car payment in the first quarter.

On the other end of the income and balance sheet spectrum, spending has been bolstered by massive wealth gains since the “Fed Pivot” towards rate cuts in November 2023. Since that time, stock market wealth gains have continued to fuel discretionary purchases. In contrast to lower-income households who struggle to service their debts, higher interest rates have furthered the windfall for wealthier Americans who own savings accounts and money market funds. One corroborating data point: 20% of the U.S. population is planning a foreign vacation within the next six months—an all-time record.

For the economy as a whole, the rising wealth of middle- and high-income households appears to be largely offsetting the harmful effects of larger debt service for those of fewer means. Another economic buttress: private equity and private credit funds are providing much of the capital for distressed firms. To the extent that companies are getting into trouble, access to these sources of funds has enabled them to reorganize their debts, rather than ceasing operations and liquidating assets.

As we’ve previously suggested, barring a major international event (e.g., terrorist attack or pandemic), we’d expect any recession to be relatively mild, given the aggregate strength of household balance sheets and accommodating fiscal policy.

Asset Class & Sector Survey

The correlation between the S&P 500 Index and its constituent stocks is also near a 25-year low. In so many words, if the Index is a proxy for “the stock market” and most stocks aren’t trading in line with the Index, then “stock returns” will likely remain beholden to the largest companies for the foreseeable future.

Consensus earnings growth for the “Magnificent Seven” stocks is a staggering 30% for fiscal 2024. For the “Other 493,” earnings expectations are far more moderated (7%). In fact, earnings for the “S&P 493” haven’t realized year-over-year growth since Q4 2022.

The top 10 companies in the S&P 500 make up 35% of the market value but only 23% of earnings. This disparity between the two measures is at an all-time high, meaning that the S&P 500’s valuation is reliant not only on a record-low number of companies, but also record-high bullishness on their future earnings.

Extreme market concentration and low correlation are problematic enough, but lofty valuations further compound the issue. Barring the Great Financial Crisis (when profits collapsed), today’s trailing price-to-earnings multiple is the highest for any quarter since the tech bubble of the late 1990s. If Index returns are going to continue their unimpeded run, the lofty earnings expectations for “The Few” will have to be realized.

Please reach out to us if you would like to discuss capital markets or your personal financial plan.

Teancum D. Light, JD, CPA, CFP®

Teancum D. Light, JD, CPA, CFP®

President

Chief Investment Officer

Disclosures: This material is for informational purposes only and is not rendering or offering to render personalized investment advice or financial planning. This is neither a solicitation nor a recommendation to purchase or sell an investment and should not be relied upon as such. Before taking any action, you should always seek the assistance of a professional who knows your particular situation for advice on taxes, your investments, the law or any other matters that affect you or your business. Although Lighthouse Wealth Management has made every reasonable effort to ensure that the information provided is accurate, Lighthouse Wealth Management makes no warranties, expressed or implied, on the information provided. The reader assumes all responsibility for the use of such information.