To download the PDF copy, click here: Lighthouse Wealth Management Outlook: October 2025

Riding the AI (Tidal) Wave

One can hardly open The Wall Street Journal (or any internet browser, for that matter) without encountering some new AI-related financial record. Case in point: Larry Ellison, co-founder and Chairman of Oracle, briefly became the world’s richest man last month as his company’s stock surged 40% on the announcement of its $300 billion, five-year deal with OpenAI for cloud computing capacity.

For its part, OpenAI recently held a secondary share sale of $6.6 billion by current and former employees, pushing its valuation to $500 billion. At that number, it is now the world’s most valuable private company. Equity investment and vendor financing deals with OpenAI have also exploded share prices for chip designers AMD and Nvidia and, in turn, their own vendors (e.g., Micron).

Artificial Intelligence (AI) may yet prove to be the most transformative technology of the 21st century. However, its path to changing the world will likely echo that of its historical predecessors, 19th-century railroads and 20th-century broadband, both of which involved capacity overbuild and meaningful price corrections.

Total AI capital expenditures in the U.S. are projected to exceed $500 billion in 2026 and 2027. Last week, consultants at Bain & Co. estimated that such infrastructure spending will require $2 trillion in annual AI revenue by 2030. For reference, that figure is more than the combined 2024 revenue of Amazon, Apple, Alphabet, Microsoft, Meta and Nvidia and more than five times the size of the entire global subscription software market.

For the time being, the supply of AI capabilities is growing far faster than actual use cases. The Wall Street Journal reported that American consumers spend only $12 billion a year on AI services. Currently, OpenAI has about 700 million active users each week and generates about $12 billion in recurring annual revenue. Last fall, CEO Sam Altman predicted that his company will not generate a profit until 2029 and expects to hemorrhage $44 billion before doing so (WSJ).

Although AI revenues are far smaller than the capital that is being currently invested, they may certainly grow over time to justify those investments and deliver solid returns. Unlike the internet, which required consumers and businesses to be wired for high-speed access, AI is immediately available for use by much of the planet. The pace of adoption—and revenues associated with it—may yet materialize as envisioned.

For the time being, earnings in the technology and interactive media sectors continue to grow at a staggering rate—25% annualized over the past two years. Until that growth rate starts to meaningfully decrease, bringing share prices back (or at least closer) to earth, the opportunity cost of skeptically underweighting the Big Tech giants is almost too painful to bear.

Financial Market Review

Equity markets rallied across the board in Q3. The S&P 500 gained 8.1%, with large-cap growth stocks doing slightly better at 9.8% and large value stocks posting 6.1%. Small-caps surged, with the Russell 2000 Index up 12.5%, fueled by anticipation and eventual confirmation of Fed rate cuts. Developed International indexes rose 4.5%, while Emerging Markets advanced more than 10%. The U.S. dollar firmed modestly, trimming year-to-date losses on the ICE Dollar Index from 11% to 10%.

Within the Magnificent Seven, Tesla led (40%), boosted by stronger-than-expected deliveries. Alphabet (38%) and Apple (24%) also posted robust gains, while Meta slipped 0.4%. Sector performance was broad-based: only Consumer Staples (2.6%) declined. Technology (11.5%), Consumer Discretionary (10.5%) and Communication Services (9.5%) led the advance.

The Bloomberg Commodity Index rose 2.6%, powered by precious metals: gold 17% and silver 30% in Q3. For the year, gold and silver have surged 47% and 61%, respectively—the best-performing assets of 2025. In contrast, WTI crude fell 5% while OPEC+ lifted production targets as Saudi Arabia seeks larger market share.

Bonds categorically posted positive returns as Treasury yields held steady. The Barclays Aggregate Index returned 2.1% on solid performance from corporate (2.7%) and mortgage (2.4%) bonds. Junk-rated corporate bonds posted returns in the low ~2% range. Municipal bonds went on a tear in early September, finishing the quarter up 2.75%.

Credit spreads on investment-grade corporate bonds are now at their lowest levels since 1998. Notably, two Microsoft bonds maturing in 2027 are trading at lower yields than Treasurys of the same maturity!

Source: YCharts

Economic Conditions

The Q2 GDP release is one of the oddest in recent memory. At first glance, growth looked stellar: the Bureau of Economic Analysis’ revised print was 3.8%, the largest number since late 2023. That headline strength, however, stems not from a surge in domestic vitality but from a 9% collapse in imports (a reversal of the tariff frontrunning which caused imports to spike in Q1). Consumer spending was revised higher as well, but investment and exports both weakened.

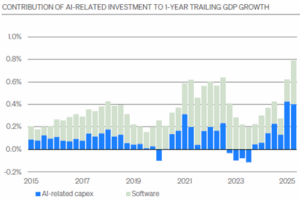

Barring the one-time import effects, real economic activity is still positive, though not stellar. Of the “real” 3% growth, AI-related capital expenditures may have accounted for about a third, according to Reuters. The heavy lifting has been done by the “hyperscalers”—Microsoft, Amazon Web Services, Alphabet, Meta and Oracle—which invested $100 billion into capex in Q2 alone, with forecasts of $400 billion over the next year.

Source: Future Standard

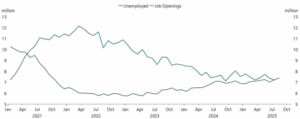

Even as economic growth continues to surprise on the upside, the labor market tells a different story. Moody’s Analytics chief economist Mark Zandi recently declared the country in a “jobs recession,” with payroll gains confined almost entirely to healthcare and hospitality. Zandi noted that September job growth was almost exclusively in California, New York and Massachusetts.

Amid restrictive immigration policies, the foreign-born workforce has dropped by 1.2 million in just six months. As a result, the labor force has stagnated, as a low 4.3% headline unemployment rate masks deeper weakness. For job seekers, conditions have clearly worsened and are more constrained. There are now 7.4 million unemployed Americans and only 7.2 million job openings—a reversal from the post-pandemic years when openings far exceeded jobless numbers. Long-term unemployment is the highest in over three years, increasingly affecting college-educated workers.

Source: Apollo Chief Economist

Employers aren’t laying off in droves, but hiring has slowed to a crawl. Executive outplacement firm Challenger, Gray & Christmas reports that hiring plans are at their weakest since 2009, while ADP data shows the private sector has shed jobs in three of the past four months.

This “slow to hire, slow to fire” dynamic has created a two-tier labor market. Workers who already have jobs enjoy relative stability and steady incomes, supporting consumer spending and resilient GDP. Those looking for work, however, face dwindling opportunities and longer job searches, particularly as AI has begun to replace human labor.

Headline CPI rose 2.9% year-over-year in August, with Core CPI at 3.1%. The Federal Reserve’s preferred metric, Core PCE, came in at 2.9%, with overall PCE inflation at 2.7%. Notably, 72% of CPI components are still rising faster than the Fed’s 2% target. Tariffs are adding fuel: the effective tariff rate has surged to 17.9%, the highest since 1934, costing families an estimated $2,400 a year.

The Fed cut the federal funds rate by a quarter point in September, bringing the target range to 4.00% to 4.25%. Chairman Jerome Powell described the move as a “risk-management cut,” underscoring signs of labor market softness. The Fed’s Summary of Economic Projections, however, delivered mixed signals: policymakers penciled in two more cuts this year and one in 2026, even as they raised their inflation forecasts.

The Fed is now firmly caught between its dual mandates of price stability and maximum employment. Inflation remains above its 2% target, with tariffs, a weaker dollar and sticky service prices threatening to keep it there for longer. At the same time, the labor market has softened enough that safeguarding jobs has clearly begun to take precedence—even as the Fed’s own forecasts project that inflation will not return to 2% until 2028.

Asset Class & Sector Survey

Given the plethora of news stories about the government shutdown, anemic labor market conditions, adverse tariff effects and inflation-driven fears pushing gold prices to new highs, it feels rather incongruous to be constructive on the stock market and economic growth. But, for the time being, the salient facts for investors are still auspicious:

- The Atlanta Fed’s GDPNow model estimates Q3 real GDP growth of 3.8%.

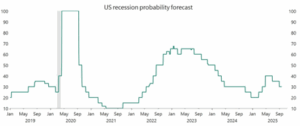

- The consensus probability of a recession over the next 12 months continues to decline and currently stands at 30%.

Source: Apollo Chief Economist

- U.S. Q2 corporate earnings were broadly positive. According to FactSet, 82% of companies beat EPS expectations, the highest percentage since 2021. Aggregate S&P 500 earnings rose 11–12% YoY.

- The “Magnificent Seven” delivered 26.6% YoY growth in Q2 (FactSet), while the other 493 companies managed a more modest 4% (GSAM / BlackRock).

- The median forward P/E ratio across the “Magnificent Seven” is 27 times, roughly half the equivalent valuation of the biggest seven companies in the late 1990s (Goldman Sachs).

More than anything else, bond trading is an exercise in quantitative discipline. Consequently, the aforementioned 27-year-low on credit spreads made our decision to reduce our clients’ corporate bond exposure an easy call to make. (We’re down from about 70% to 50% in our taxable fixed income models.)

In contrast, stocks are far trickier—in the short run, their prices are far more susceptible to investor mood swings than bonds. But over the long run, stock values are driven primarily by earnings growth. With a revolutionary technology now propelling a third of U.S. GDP growth and three-quarters of the earnings growth in major indexes, forecasting that trajectory has become a difficult exercise indeed. For now, we’ll keep surfing the AI wave with index-level weightings, but we’ll remain vigilant for signs of a potential wipeout.

Please reach out to us if you would like to discuss capital markets or your personal financial plan.

Teancum D. Light, JD, CPA, CFP®

President

Chief Investment Officer

Disclosures: This material is for informational purposes only and is not rendering or offering to render personalized investment advice or financial planning. This is neither a solicitation nor a recommendation to purchase or sell an investment and should not be relied upon as such. Before taking any action, you should always seek the assistance of a professional who knows your particular situation for advice on taxes, your investments, the law or any other matters that affect you or your business. Although Lighthouse Wealth Management has made every reasonable effort to ensure that the information provided is accurate, Lighthouse Wealth Management makes no warranties, expressed or implied, on the information provided. The reader assumes all responsibility for the use of such information.