Download a PDF version of the Lighthouse Wealth January Outlook

Economic Conditions

We write our inaugural newsletter amidst unique economic and capital markets circumstances. A global pandemic ravaged the world’s economies in the second quarter of 2020, sending real Gross Domestic Product (GDP) down by more than 30% [1]–the deepest quarterly drop in the history of the United States–as unemployment rates spiked into the mid-teens. U.S. stock markets decreased by over 30% within a month [2], their steepest drop in history. All the ingredients of a protracted recession and bear market were in place.

And then the United States Treasury stepped into the fray.

Though the final numbers are weeks away, the total amount of federal deficit spending in 2020 is projected to be in the neighborhood of 16%-18% [3] of GDP. To put that in perspective, the Treasury’s deficit was 20% in 1945 [4], the year World War II ended. The 10% deficit spending related to the Global Financial Crisis in 2009 [5] seems downright modest by comparison.

While the Treasury Department was busy making stimulus deposits into individual and business checking accounts, the Federal Reserve was cutting interest rates to zero and buying bonds at a furious pace (albeit below that of 2008). Year to date, the Fed has increased its balance sheet by 75% [6]. More importantly, the Fed took the unprecedented (yes, that word is warranted in this case) step of creating facilities to purchase corporate bonds, including junk-rated bonds.

As a result of these actions and similar steps taken by other governments, we are left in the following set of conditions:

- A depression was averted.

The Federal Reserve now expects real Gross Domestic Product to decrease by only -2.4% in 2020 [7]. Previous estimates by the Federal Reserve and International Monetary Fund had been closer to -4% [8], a level unseen since the end of WW II. The Fed also upped its 2021 real GDP forecast to +4.2% from +4.0% [9].

- There are 25% more U.S. dollars in circulation today versus December 2019. [10]

As the Treasury deposited money into checking accounts through stimulus programs and the Federal Reserve created dollars to purchase newly issued Treasury bonds, the money supply increased accordingly.

- The government has effectively set a floor for the prices of risk assets.

Between rock bottom interest rates and flat-out bond purchases, markets have become dependent on Federal Reserve support.

Financial Market Conditions

S&P 500 companies’ earnings barely budged in 2019 and dropped about 14% in 2020 [11]. Notwithstanding depressed economic conditions, the U.S. stock market has still managed to generate a 50% gain over the past two years [12].

On the surface, this catapult in prices is completely unwarranted. Even if the more sanguine earnings projections are realized in 2021, it still represents only a 4% increase versus 2019 [13]. By virtually all metrics, stocks are trading at lofty valuations, and those of recent IPOs are at their highest levels since the dot-com bubble.

The primary supports to stock prices are expectations for a post-COVID recovery in economic activity, and the aforementioned fiscal and monetary policies. To the latter, the Fed has committed to buying at least $120 billion of bonds each month and keeping short-term interest rates near zero until 2023. It has also reaffirmed its 2% long-term inflation target, and even above that level in the short run [14]. Inflation-protected bonds are currently prognosticating inflation rates in that range over five- and ten-year horizons [15].

Before the Global Financial Crisis, a 25% increase in the money supply would have been expected to generate a commensurate increase in consumer prices. Times have changed though, as the massive increase in money demand has provided an effective offset. However, the respective 25%, 50%, and 290% rise in gold, silver, and bitcoin prices in 2020 [16] demonstrate at least some skepticism about how long inflation can be contained with so much additional money in circulation.

Given their present lofty valuations, the case for owning stocks boils down to four major factors:

- Politicians of both major parties are perfectly willing to run large, long-term deficits.

- The Federal Reserve is wholly committed to 2% inflation.

- Higher consumer prices are ultimately reflected in higher corporate earnings.

- Bond yields are paltry.

According to Deutsche Bank, only about 55% of the bonds in the world are yielding more than 1%, and only about 15% have a yield above 2%. The implication is that, absent a major shift in government policy, most bondholders are virtually guaranteed to lose purchasing power over the next decade. At these rates, even a small increase in yields causes a steep decrease in bond prices.

The rising government tide that has lifted all asset prices isn’t likely to recede anytime soon. But starting valuations imply that U.S. stock investors still shouldn’t expect more than mid-single-digit returns over the next five years. The easy money has been made and defensive posturing is now warranted.

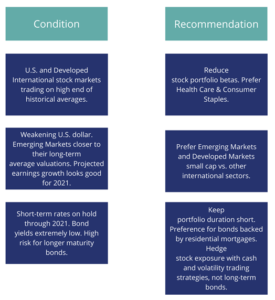

Portfolio Positioning

Below, we summarize our assessment of capital market conditions and corresponding recommendations:

If you would like to discuss any of the above topics or how they might apply to your financial plan, please don’t hesitate to reach out to me.

Best wishes for a prosperous 2021!

Disclosures: This material is for informational purposes only and is not rendering or offering to render personalized investment advice or financial planning. This is neither a solicitation nor a recommendation to purchase or sell an investment and should not be relied upon as such. Before taking any action, you should always seek the assistance of a professional who knows your particular situation for advice on taxes, your investments, the law or any other matters that affect you or your business. Although Lighthouse Wealth has made every reasonable effort to ensure that the information provided is accurate, Lighthouse Wealth makes no warranties, expressed or implied, on the information provided. The reader assumes all responsibility for the use of such information.

Sources:

[1] fred.stlouisfed.org/series/GDP. Retrieved January 8, 2021.

[2] YCharts.com. Retrieved January 10, 2021.

[3] Davidson, Kate. “U.S. Budget Gap Tripled in Fiscal 2020 as Government Battled Pandemic.” The Wall Street Journal. Oct. 8, 2020.

[4] www.thebalance.com/us-deficit-by-year-3306306. Retrieved January 10, 2021.

[5] Ibid

[6] YCharts.com. Retrieved January 10, 2021.

[7] fred.stlouisfed.org. Retrieved January 8, 2021.

[8] cnbc.com/2020/12/16/fed-raises-its-economic-outlook-slightly-sees-4point2percent-growth-next-year-and-5percent-unemployment-rate.html. Retrieved January 8, 2021.

[9] Ibid

[10] YCharts.com. Retrieved January 10, 2021.

[11] Ibid

[12] Ibid

[13] Ibid

[14] Timiraos, Nick. “Fed Saw Bond-Buying Program Providing ‘Very Significant’ Support.” The Wall Street Journal. January 6, 2021.

[15] YCharts.com. Retrieved January 10, 2021.

[16] YCharts.com. Retrieved January 8, 2021.