Download a PDF copy of the Lighthouse Wealth Outlook here: Lighthouse Wealth Outlook – January 2022

Economic Conditions

Real U.S. Gross Domestic Product (GDP) rose 2.3% in the third quarter, the weakest quarterly number since the COVID-19 pandemic broke in Q2 2020.[1] Strained global supply chains and a decline in federal government pandemic relief money were key factors weighing on growth. The Federal Reserve now projects full-year 2021 GDP growth at 5.5% (down from its 5.9% September estimate), with a 2022 growth of 4.0%.[2]

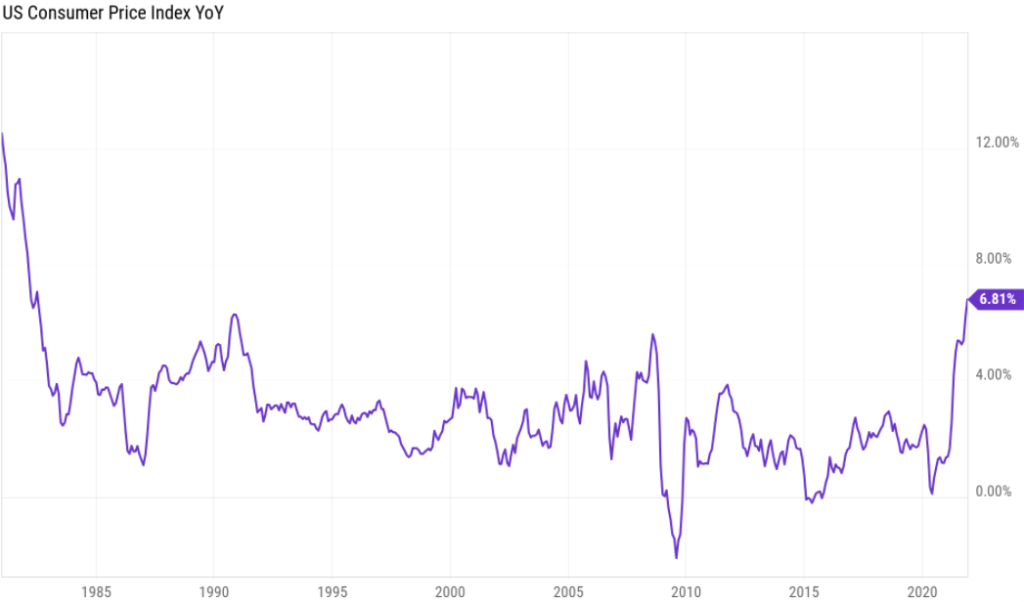

As the economic growth escalates, so do price levels. In November, the Consumer Price Index spiked 6.8% on a year-over-year basis. It was the largest such increase since early 1982.[3]

Core inflation, which excludes food and energy, was up 4.9% in November, a 30-year high. The Producer Price Index jumped 9.6%, up from an 8.6% rise in October, and the largest increase since the data was first calculated in 2010.[4]

Listed are a few other noteworthy inflation data points:

- Used-car prices rose at a 31.4% annual rate in November.[5]

- Median rental rates increased 11% in 2021.[6]

- Social Security check recipients will see a 9% increasein their monthly payments this year, the biggest annual raise since 1982.[7]

- The standard cost for Medicare Part B is jumping 14.5% to $170.10 per month.[8]

- Food prices are estimated to rise 5% in the first half of 2022.[9]

- The Pennsylvania Turnpike Commission approved a 5% toll increase for 2022 in the summer.[10]

The Federal Reserve Bank of New York’s Survey of Consumer Expectations shows heightened anxiety about the rate of inflation. Median expectations for the coming year are a 6.0% increase in prices, with a 4.0% annual increase anticipated over the next three years.[11]

The quickening pace of rising prices is also beginning to disquiet some investors. An Allianz survey found that 25% of Americans see rising inflation as the single biggest threat to their retirement plans, compared to 8% a year ago.[12]

Financial Market Conditions

From a stock investor’s standpoint, 2021 was “as good as it gets.” The S&P 500 posted a massive 28.7% return, with only a 5% peak-to-trough decline over the course of the year.[13] Once again, U.S. shares led the world, with the MSCI Europe Australia Far East Index returning 11.5%, as Emerging Markets indices fell about 4%.[14] In particular, Asian stocks have suffered losses due to ongoing economic effects of COVID-19.

At 32%, large growth stocks posted the best returns among equity styles. Mid-cap and small-cap growth companies did not fare as well, returning 13% and 3% respectively. Value stocks did well across the board with large-cap value up 25%, as mid-cap and small-cap value shares were both up 28%.[15]

Often touted as a hedge against inflation, gold managed to lose over 4% in 2021, putting it at least 12% behind the Consumer Price Index. (In all fairness, gold was the best-performing major asset class in 2020 when it was up 25%.) Other commodities fared much better, though, as the Bloomberg Commodity Index rose 27%.[16]

Treasury Inflation Protected Securities (TIPS) were 2021’s best-performing fixed-income sector, with total returns in the 5-6% range. TIPS yields hit an all-time low recently, with five-year maturities bottoming at -1.91% in November. Five-year TIPS are currently yielding -1.6%. So long as inflation exceeds that number, and yields do not rise, TIPS are still capable of providing a positive return in 2022.[17]

In addition to TIPS, risky credit sectors (i.e., junk bonds and bank loans) also generated positive returns in 2021 as interest payments in the 4-5% range offset very modest price declines. Investment-grade sectors fared far worse, with the Bloomberg U.S. Aggregate Index down more than 1.5% and corporate bond indexes generally down near 2%. It was the worst annual showing for investment-grade bonds since the “taper tantrum” of 2013.[18]

Portfolio Positioning

As we reconsider the outlook, we penned this time a year ago, there was one story we got overwhelmingly right in 2021: The Federal Reserve’s commitment to stoking inflation, coupled with paltry yields, made long-term bonds a terrible wager. We find little reason to change our opinion at this juncture.

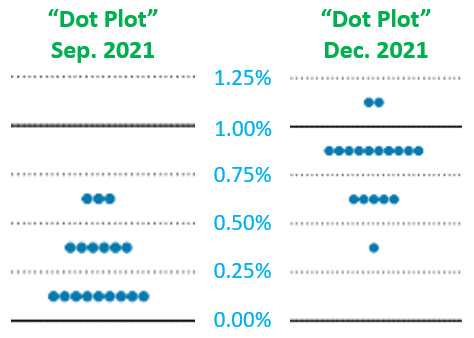

To the Federal Reserve’s credit, it is now acknowledging the high inflation prints and indicating that three 0.25% interest-rate increases are on deck for 2022. (As recently as September, the Federal Reserve was projecting only one 0.25% rate hike for this year.) But contrary to the signals from the Producer Price Index, TIPS market, and its own Survey of Consumer Expectations, the Federal Reserve is forecasting a 2022 inflation rate of only 2.6%.[19]

This projection strikes us as unrealistically low. In his press conference on December 15th, Chairman Jay Powell told a reporter that, notwithstanding the elevated inflation readings, the Federal Reserve would not taper its monthly asset purchases more quickly due to potential adverse market reactions. In so many words, Powell more or less admitted that he is more concerned about provoking a stock market correction than about corralling high inflation.[20]

Source: www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20211215.pdf

After a blistering run-up in 2021, making any constructive arguments for U.S. stocks feels rather counterintuitive, particularly given that the Federal Reserve has signaled that monetary conditions will begin to tighten. However, we note that the forward price-to-earnings ratio for S&P 500 companies is slightly below where it was a year ago.[21] That is, this year’s massive run-up in large-cap stocks was driven by earnings, not multiple expansion.

We also note that, despite generally lofty valuations, there are some sectors that are not terribly overpriced versus historical averages, namely value stocks and the healthcare sector. For income-minded investors, we would generally encourage holding some combination of low-volatility REIT’s, short-duration mortgage bond funds and cash in lieu of longer-duration bonds.

Disclosures: This material is for informational purposes only and is not rendering or offering to render personalized investment advice or financial planning. This is neither a solicitation nor a recommendation to purchase or sell an investment and should not be relied upon as such. Before taking any action, you should always seek the assistance of a professional who knows your particular situation for advice on taxes, your investments, the law or any other matters that affect you or your business. Although Lighthouse Wealth has made every reasonable effort to ensure that the information provided is accurate, Lighthouse Wealth makes no warranties, expressed or implied, on the information provided. The reader assumes all responsibility for the use of such information.

[1] www.businesstimes.com.sg/government-economy/us-q3-economic-growth-revised-slightly-higher

[2] www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20211215.pdf

[3] www.barrons.com/articles/inflation-rising-prices-remain-elevated-51639500810

[4] ibid

[6] inman.com/2022/01/03/us-median-rent-rose-11-in-2021-due-to-inflation/

[7] cbsnews.com/news/social-security-cola-cost-living-increase-inflation-january-2022/

[8] ibid

[9] wsj.com/articles/these-food-items-are-getting-more-costly-in-2022-11640601008

[10] www.paturnpike.com/news/details/2021/09/16/20210706153011

[11] www.newyorkfed.org/newsevents/news/research/2021/20211213

[12] www.allianzlife.com/about/newsroom/2021-press-releases/rising-inflation-seen-as-biggest-risk-to-retirement-plans-in-2022

[13] YCharts. Retrieved January 5, 2022.

[14] ibid

[15] ibid

[16] ibid

[17] ibid

[18] ibid

[19] www.federalreserve.gov/mediacenter/files/FOMCpresconf20211215.pdf

[20] ibid

[21] YCharts. Retrieved January 5, 2022.