Download a PDF copy of the Lighthouse Wealth Management: Outlook – April 2023

“What, me worry?”

The United States recently witnessed the second and third largest bank failures in its history: Silicon Valley Bank and Signature Bank.

With assets of $209 billion, Silicon Valley Bank (SVB) was about two-thirds as large as Washington Mutual (WaMu) was when it failed back in 2008. But, unlike WaMu, SVB’s balance sheet was not laden with delinquent loans. Rather, SVB’s collapse stemmed from two different problems: declines in the value of its long-term Treasury bonds and deposit flight. As concerns over 20 – 30% unrealized losses in its Treasury portfolio spread like wildfire among the technology firms and executives who banked there, a huge swath of SVB’s uninsured deposits quickly took flight.

SVB’s failure, and the closure of the cryptocurrency-linked Silvergate Bank (Silvergate) a week earlier, fanned depositor fears at NYC-based Signature Bank (Signature). Like Silvergate, Signature had significant ties to the cryptocurrency industry. Similar to SVB, a significant share of Signature’s deposits were uninsured (93%). Unable to meet an avalanche of withdrawal demands, it was quickly seized by its regulators.

To prevent a broader contagion, the Treasury, the Federal Reserve (the “Fed”) and the Federal Deposit Insurance Corporation (FDIC) issued a joint statement on March 12, 2023, invoking “a systemic risk exception” for both SVB and Signature banks. Regulators waived the $250,000 FDIC limit on deposit insurance and guaranteed all deposits. The Fed went a step further, creating a new facility to lend against “high-quality securities” at their par value (even if their market values were significantly lower). The new Bank Term Funding Program (BTFP) is backstopped by up to $25 billion from the Treasury.

If the past four weeks are any indication, the updated federal safety net has largely abated depositor fears. But even if that constituency has been reassured, investors and economists still have plenty to worry about.

After a near collapse, major global bank, Credit Suisse, was forced into a merger on March 19, 2023. The Wall Street Journal noted that the equity risk premium—the gap between the S&P 500’s earnings yield and that of 10-year Treasury—is around 1.6%, a low not seen since October of 2007.[1] Corporate earnings results and 2023 outlooks are weak at best, and every time-tested recession indicator is flashing yellow (if not red).

Readers of a certain age will remember Mad magazine. For decades, Mad was the go-to publication for adolescents seeking subversive humor. Nearly every cover featured a freckled, mussy-haired mascot, Alfred E. Neuman. No matter how ridiculous or perilous his setting, young Alfred could always be counted on to muster an imbecilic, gap-toothed grin. On occasion, he would utter his signature catchphrase: “What, me worry?”

Given the present circumstances, it is not terribly hard to imagine that Alfred E. Neuman somehow finagled his way into the Nasdaq stock exchange mid-March, began fumbling with the controls and pushed stock prices skyward. How else do you explain a big market rally amidst all these considerable causes for concern?

Financial Market Review

After declining 18% last year, the S&P 500 Index rebounded in the first quarter 2023, gaining 7.5%. The gains were concentrated in the Communications (21%), Technology (22%) and Consumer Discretionary (16%) sectors. Apple, Microsoft, Amazon, NVIDIA, Meta, Alphabet and Tesla were the primary drivers. Without those big names, the S&P 500 Index would have been flat in the first quarter. (By comparison, the Dow Jones Industrial Average was up only 0.9%.)

Financial Services (5.5%) was the biggest sector laggard. While stocks of mega-banks like Wells Fargo (down 8.9%) and Bank of America (down 13.1%) posted negative returns, smaller banks fared much worse. Fears of deposit flight and higher interest costs on checking and savings accounts sank shares of regional banks by 20-25% for the quarter. Energy (down 4.3%) and Heath Care (down 4.3%) also posted negative returns.

The banking turbulence also weighed on the global IPO (initial public offering) market. During the first quarter, 299 companies went public, raising $21.5 billion, down 8% and 61% year-over-year, respectively. Declining valuations for smaller technology companies, often cash-flow negative, have further reduced the appetite for public listings. Venture capital funding worldwide also declined 53% in the first quarter of this year, according to data from Crunchbase.

Expectations for a summer pause in Federal rate hikes caused the U.S. dollar to fall modestly versus most major currencies in the first quarter. This helped push developed international stocks up 9%. Emerging markets were up 4%.

Bonds rebounded from their worst calendar year on record, as expectations for a less-aggressive Fed pushed the 10-year Treasury yield down by 0.4%. All bond sectors rallied as the Bloomberg Aggregate Bond Index gained 3.2% in the quarter.

Falling interest rates and concerns over bank stability boosted gold prices, which climbed 8% in the first quarter. Other commodities fared worse; the Bloomberg Commodity Index was down 5.4%.

Economic Conditions

The final fourth quarter gross domestic product (GDP) number was 2.6%, following a GDP increase of 3.2 % in the third quarter. The Atlanta Federal Reserve is currently projecting first quarter GDP of 2.2%. The International Monetary Fund (IMF) is less sanguine, expecting growth of only 1.6% for all of 2023.

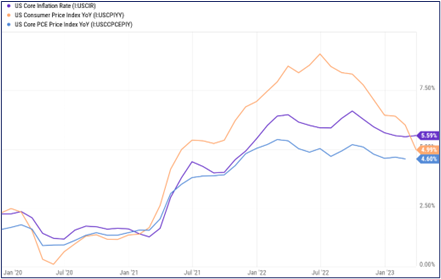

The Consumer Price Index (CPI) rose 5% year-over-year in March, down from February’s 6% pace and December’s 7% print. Although CPI, the headline rate of inflation, is falling, the slower rate of decline in the Core CPI—which excludes volatile food and energy prices—has slowed less quickly. Core CPI is generally considered to be a more reliable indicator of the long-term trend in inflation.

Similarly, the Fed’s favorite inflation metric, the Core Personal Consumption Expenditures Price Index (Core PCE), is only down modestly from its February 2022 highs. At 5.6% and 4.6%, respectively, Core CPI and Core PCE are both well above the Fed’s 2% long-term target.

Source: YCharts

After the Fed raised its benchmark interest rate to a 4.75% – 5.00% range in late March, Chairman Jerome Powell stated that there were other forces at work to slow inflation besides the Fed’s own interest-rate hikes. “It can come from tighter credit conditions,” Powell remarked.

“Tighter credit conditions” refers to more stringent underwriting and a slowdown in loan origination volumes. As credit-dependent industries (e.g., construction and manufacturing) find it more difficult and expensive to borrow, their reduced output in turn reduces the demand for other goods and services which they consume. A general business slowdown (i.e., a recession) then typically follows.

According to the Fed’s most recent Senior Loan Officer Opinion Survey on Bank Lending Practices in January, banks reported reduced demand for all types of commercial real estate loans, commercial and industrial loans and household loans.[2] At the same time, when loan demands were falling, banks were reducing supply by tightening their lending standards.

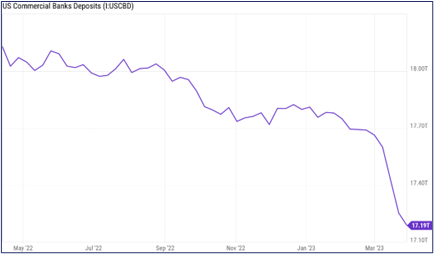

At least some of the tighter lending standards is due to less loanable funds. As depositors have been seeking higher interest yields and safety, many of them have drawn down their bank balances in favor of money market funds which own Treasury bills and high-quality commercial paper. While smaller banks have been hit the hardest, total deposits at all U.S. banks are at their lowest level since September of 2021.

Source: YCharts

We find it difficult to disagree with the majority of surveyed banks, which are projecting a 40–80% probability of a recession in the following year. In addition to the tightening credit conditions, another time-tested recession indicator is flashing yellow: the Treasury yield curve. Inverted since last July, the yield curve finally started to “de-invert” several weeks ago. After being above 5% in early March, the two-year Treasury yield fell below 4%. Such de-inversion usually occurs several months before a recession unfolds.

Asset Class & Sector Survey

“The stock market is not the economy” is a truism that bears repeating. While the two are inextricably intertwined, it is often the case that one temporarily moves in a different direction than the other, which seems to be what has been happening in recent weeks. Even with the tech giants that drove much of the stock market’s fantastic first quarter return, soft sales and earnings are more consistent with a recession that appears to be getting underway.

The data is clear that the COVID-era demand for PC sales (and the attendant components) are in a cyclical decline. Apple Inc.’s computer shipments plunged by 40% and Lenovo Group and Dell Technologies Inc. recorded drops of more than 30%. Shipments were down 24% at HP.

Apple Inc. saw its quarterly revenue decrease by 5.5% versus a year ago (even with an extra week in the quarter), from weakness in iPhone and Mac sales. At Meta Platforms (Facebook), sales were down 4%, with further downward guidance for the second quarter. Sales hardly budged at Alphabet (Google); Microsoft’s sales gain was a paltry 2%.

We might be more constructive on stocks if the lackluster earnings outlooks were already factored into share prices; however, they do not appear to be. At 18.6 times forward earnings and 21 times trailing earnings on the S&P 500 companies, equity pricing still seems elevated, particularly given that 10-year investment grade corporate bonds are paying north of 5%. Given the bearish headwinds, the risk premium is too small to warrant adding meaningfully to existing stock positions.

As we see it, counting on lower interest rates to buttress stock prices is a risky bet. If the economy did meaningfully turn south and the Fed began reducing rates, stock prices would likely reflect a material decline in corporate earnings. Alternatively, if the economy does manage to hold up, then the Fed would be much less inclined to reduce interest rates before year end, as core inflation is still two and a half times its target level. Those higher interest rates would provide a drag on stock prices.

One additional reason for bearishness: in the last 12 bear markets (excluding the current one), stock prices never bottomed until the National Bureau of Economic Research (NBER) declared a recession. We are not there yet.

For the time being, we are not concerned about a 2008-style cascade of financial institution collapse, nor the security of our clients’ cash positions with our custodian. To the extent that inflation persists, and we see a “higher-rates-for-longer” Federal Reserve, we would look to tactically lengthen bond maturities if the 10-year Treasury yield reapproaches 4%. For those interested in maximum safety, taxable money market funds holding U.S. Treasury bills are currently paying 4.5%. That is a nice worry-free rate of interest.

Please reach out to us if you would like to discuss capital markets or your personal financial plan.

Teancum D. Light, JD, CPA, CFP®

Teancum D. Light, JD, CPA, CFP®

President

tlight@lighthousewealth.com

Chief Investment Officer

jadams@lighthousewealth.com

Disclosures: This material is for informational purposes only and is not rendering or offering to render personalized investment advice or financial planning. This is neither a solicitation nor a recommendation to purchase or sell an investment and should not be relied upon as such. Before taking any action, you should always seek the assistance of a professional who knows your particular situation for advice on taxes, your investments, the law or any other matters that affect you or your business. Although Lighthouse Wealth Management has made every reasonable effort to ensure that the information provided is accurate, Lighthouse Wealth Management makes no warranties, expressed or implied, on the information provided. The reader assumes all responsibility for the use of such information.

[1] Souce: https://www.wsj.com/articles/stocks-havent-looked-this-unattractive-since-2007-78fc374c

[2] Source: https://www.federalreserve.gov/data/sloos/sloos-202301.htm