Download a PDF copy of the Lighthouse Wealth Management: Outlook – October 2023

“You only live twice, Mr. Bond.”[1]

In 1967, James Bond fans were startled to see their hero fatally betrayed within the first five minutes of “You Only Live Twice.” To their relief, they soon learned that 007 had merely faked his death. No one could have dispatched Bond that easily. (Obviously.)

Five-plus decades and as many actors later, Bond showed his flexibility. He could be portrayed in a more whimsical, tongue-in-cheek fashion, à la Roger Moore or Pierce Brosnan. Alternatively, he could be played in a dark, serious tone, as Daniel Craig so ably demonstrated. On occasion, he might even order a whisky in lieu of his trademark vodka martini or opt for a tricked-out BMW rather than an Aston Martin.

But moviegoers knew the hard-and-fast rules of the franchise. In every outing, Bond was assuredly going to drive ultra cool cars, epitomize male fashion, romance beautiful women and thwart imposing henchmen—charmingly skirting the authority of his superiors at MI6 along the way. Whatever else might transpire, the megalomaniac villain was never going to win in the end. And Bond was always going to survive.

The film producers essentially rebooted the franchise when Daniel Craig first assumed the role in Casino Royale and concluding his tenure with an onscreen death was always a possibility. But then again, this was Bond, and there were certain boundaries that even filmmakers wouldn’t dare to cross—right?

Dare they did. “No Time to Die” lived up to the irony of its title. We, the incredulous, distraught viewers had two major consolations, though. Our hero had gone out in as much of a graceful, stoic, self-sacrificing form as we could have hoped, and we could cling to the promise, made once again, in the film’s closing credits: “James Bond will return.”[2]

In retrospect, Bond’s onscreen demise in October of 2021 was eerily prophetic of a shared fate with his capital markets counterpart: “Bond. Long Bond.”

Since the premiere of “No Time to Die,” the Bloomberg US Long Treasury Index has lost 30%. Barring a course correction before New Year’s, bonds are now on track for an unprecedented negative return for three consecutive calendar years. However you measure it, we are experiencing the worst bond market of all time.

All this makes us long for the good old days, when you could always count on nothing “too bad” ever happening to Bond. Or to bonds.

Financial Market Review

After closing July at a 16-month high, the S&P 500 lost 6.6% over the final two months of Q3 to finish down 3.2%. Energy (up 12.1%) was the big winner, as crude oil prices climbed 30%. Communication Services was also positive (up 1.0%), on solid performance from Alphabet and Meta. All other sectors posted a decline.

Thanks to Alphabet, Meta and Invidia, large cap growth was the best-performing sector in Q3, even as the other four “Magnificent Seven” large growth stocks declined. In contrast, mid- and small-cap growth companies fared worse than their value sector counterparts.

High American interest rates have attracted overseas investors, causing a U.S. dollar rally against all major currencies. The ICE U.S. Dollar Index was up 3.2% for the quarter. The rising dollar weighed on international stocks, whose indexes were down by 4-5%.

Crude oil prices spiked from $70 a barrel in late June to above $90 by Labor Day, driven by production cuts by Saudi Arabia and Russia. That $20 change was the second-highest quarterly increase since 2008 (surpassed only by Q1 2022). In contrast, precious metals prices dropped, with gold and silver down 4% and 3%, respectively.

Bonds had an abysmal quarter as the 10-year Treasury yield climbed 0.8% to north of 4.6% (a new 16-year high), despite declining core inflation numbers. Long Treasurys fared even worse, with 30-year yields rising almost 1% in the space of 90 days! The Bloomberg Aggregate Bond Index lost 3.2%.

Floating-rate bank loans and short-term corporate bonds did well, however, as credit spreads (yields in excess of comparable maturity Treasurys) held firm, resulting in a positive total return in Q3.

Source: YCharts

Economic Conditions

The Commerce Department released its final revision of Q2 real gross domestic product (GDP) in September. Headline GDP increased at an annual rate of 2.1% in Q2 2023, largely in line with previous estimates. However, personal consumption, which comprises 70% of GDP, grew at only 0.8%, less than half of expectations and down from 3.8% in Q1. The fall in consumer spending was offset by stronger business spending, which grew by 7.4% in the quarter.

Inflation is still running high, although the pace of price increases has begun to taper off. The Consumer Price Index rose 3.7% in August, with much of the increase driven by the retail price of gasoline. Core inflation continues to drop. Core CPI rose 4.4% in August after increasing 4.7% in July.

With those core inflation rates well above its 2.0% target, the Federal Reserve elected to hold short-term rates steady at 5.25-5.50% at its September meeting. Notwithstanding the pause, the Fed’s median “dot plot” projection is for one additional rate hike in 2023, with a 0.50% cut in 2024. The projection represents two fewer rate cuts than Fed officials had predicted in June. Interest-rate futures markets are indicating a 70% probability that the Fed is done raising rates this year.

We are rather skeptical that “higher-for-longer” interest rates will be realized with target fed funds above 5% at the end of 2024, as the Fed’s September “dot plot” suggests. There are several compelling reasons to believe that a recession and consequent interest rate cuts will occur before 2025.

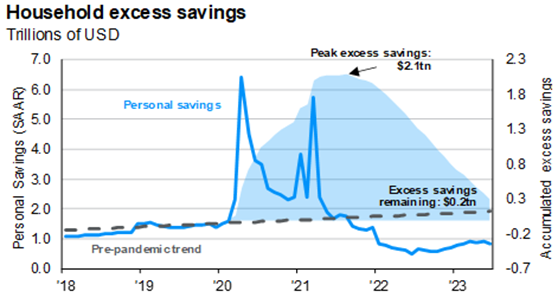

Accumulated household excess savings peaked at roughly $2.1 trillion in August 2021, due to stimulus checks and other fiscal measures during the pandemic. Since then, aggregate savings have dropped well below pre-pandemic levels, as inflation forced households to draw from savings to make ends meet. According to the Federal Reserve Bank of San Francisco, those funds were probably depleted during this quarter. We have seen similar research notes from Apollo Group and J.P. Morgan:

Source: JPMorgan

Until now, this Covid-era cash cushion has largely immunized consumers against the pain associated with rising interest rates. But student loan payments are resuming, credit card balances have risen dramatically (over $1 trillion for the first time ever) and borrowing rates have spiked (11.5% on average for a 24-month personal bank loan). The burden of debt service has begun to hit American households in earnest.

A recent Deutsche Bank analysis studied 34 past U.S. recessions to identify key warning signs. The paper highlighted four key macroeconomic triggers that have caused recessions since 1854:

- Surging inflation

- Oil price shocks

- Rapidly rising short-end interest rates

- Inversions of the yield curve

Deutsche Bank noted that while no single macroeconomic trigger can accurately predict a recession, all four of the above indicators are happening concurrently today.

We also note the implications of the dramatic change in the steepness of Treasury yield curve inversion. Although the Treasury yield curve has been consistently inverted since July 2022, (10-year yields are below 2-year yields), it’s become much less inverted recently as 10-year yields have risen. On June 30th, the difference was 1.06%. It’s at 0.32% today. Such a “bear steeping” move—when intermediate-term yields rise faster than short-term yields—is a classic indicator of a business cycle’s late stage.

Asset Class & Sector Survey

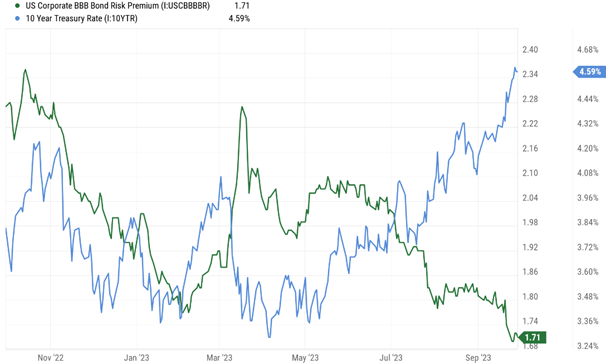

Investors often speak of a “term premium”—the additional yield offered on longer-term bonds vs. shorter-maturity instruments. This premium serves as compensation for the risks attendant with lending money for long periods of time—in particular, inflation and increasing government debt.

Since the Fed’s last major anti-inflation campaign of the early 1980’s, the term premium has been in a secular decline. But since late 2022, the yield demanded by investors to hold 10- and 30-year bonds has increased markedly. However, long-term inflation expectations (the blue line in the graph below) don’t appear to be driving this rising term premium.

Source: YCharts

If inflation worries aren’t the culprit behind the recent spike in long-term interest rates, then what’s causing this phenomenon? Falling demand and higher supply of Treasury bonds.

On the demand side:

While it’s an oft-repeated trope that Japan and China hold a huge swath of U.S. government debt, those two governments collectively hold less than 8% of outstanding Treasurys—the lowest percentage in over 20 years. In absolute terms, China recently cut its Treasury portfolio to the lowest level since 2009.

Along with Asian central banks, the Federal Reserve’s appetite for Treasury bonds has also decreased. The Fed has reduced its balance sheet by $1 trillion since last July—right around when the term premium really took off.

Other investors may be more cautious on long-term Treasurys after Fitch Ratings’ recent downgrade of U.S. government debt from AAA to AA+. Fitch cited fiscal deterioration over the next three years, growing national debt and the erosion in standards of governance over the last 20 years (including repeated occurrences of debt-limit political standoffs).

On the supply side:

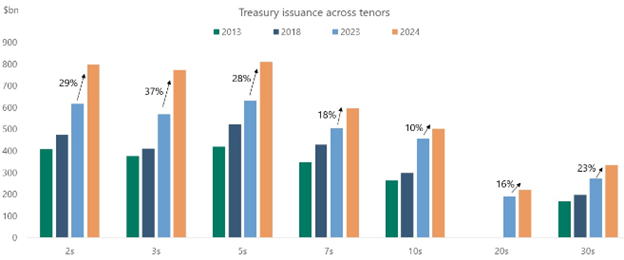

Uncle Sam’s borrowing needs and refinancing costs are rising sharply. The federal budget deficit is likely to be 6% of GDP this year. According to the Congressional Budget Office, net interest payments alone this coming fiscal year will be $745 billion. In 2024, Treasury auction sizes are set to increase considerably across all maturities—23% on average.

Source: Apollo Group

Regardless of the relative contributions of the above factors, the pertinent questions for investors are:

- Are we receiving sufficient yield for intermediate- and long-maturity bonds—i.e., is the risk premium high enough yet? Could bond prices get beat up even more?

- Given today’s bond yields, how do stocks and other asset classes look by comparison?

At 2.40%, inflation-adjusted 10-year Treasury yields are at their highest levels since the Global Financial Crisis. Coupled with a probable recession by 2025, now would seem to be a reasonable entry point for investors. The “X factor” of the Fed’s balance sheet reduction will likely prove the decisive one for bond performance, though.

As to the relative value of bonds vs. stocks, it’s hard to prefer the latter. As we have observed previously this year, corporate earnings have been declining for several quarters. Given the adverse effects of higher labor, energy and interest costs, coupled with a diminished money supply, the earnings outlook is not likely to improve anytime soon. And stock valuations remain uncompelling.

For the time being, we remain reluctant to add equity exposure for another reason: stocks moving too much in tandem with bonds, so there’s little (or no) diversification benefit. Since 2022, there have been four quarters when stocks and bonds both lost 2.5% or more. The correlation between the two asset classes is now approaching the 25-year high it reached in 2020.

We don’t pretend to know when Bond will return to the screen, or when bonds will start generating positive returns once again. The former is up to Eon Productions; the latter is largely up to the Fed. In both cases, we’d prefer it to be sooner rather than later.

Please reach out to us if you’d like to discuss capital markets or your personal financial plan.

Teancum D. Light, JD, CPA, CFP®

President

tlight@lighthousewealth.com

Chief Investment Officer

jadams@lighthousewealth.com

Disclosures: This material is for informational purposes only and is not rendering or offering to render personalized investment advice or financial planning. This is neither a solicitation nor a recommendation to purchase or sell an investment and should not be relied upon as such. Before taking any action, you should always seek the assistance of a professional who knows your particular situation for advice on taxes, your investments, the law or any other matters that affect you or your business. Although Lighthouse Wealth Management has made every reasonable effort to ensure that the information provided is accurate, Lighthouse Wealth Management makes no warranties, expressed or implied, on the information provided. The reader assumes all responsibility for the use of such information.

[1] Lewis G. (Director). (1967). You Only Live Twice [Film]. Eon Productions.

[2] Cary Joji F. (Director). (2021). No Time to Die [Film]. Eon Productions.