Download a PDF copy of the Lighthouse Wealth Outlook here: Lighthouse Wealth Outlook – October 2021

Economic Conditions

U.S. Gross Domestic Product (GDP) rose 6.7% in the second quarter, up modestly from its 6.4% pace in Q1[1]. For the full year 2021, the Federal Reserve is forecasting real GDP growth of 5.9%, then declining to 3.8% for 2022.[2]

Notably, the Fed’s current projection for 2021 GDP is down a full percentage point from its June estimate.[3] The downward revision to the growth forecast is the result of expectations for lower output from continued supply chain congestions, ongoing labor shortages, and possible COVID surges.

Concurrent with lower growth projections is an attendant increase in inflation. The Consumer Price Index (CPI) rose 5.3% year over year in August. “Core CPI,” which excludes food and energy prices, was 4.0% higher.[4] The Federal Reserve now forecasts core inflation of 3.7% for 2021 (up from its 3.0% prediction in June), then moderating to 2.3% in 2022.[5]

For the time being, inflation shows little signs of abating. Producer prices rose a staggering 8.3% in August versus year-ago levels—their fastest annual pace on record for the fifth consecutive month.[6] Oil prices have climbed back near pandemic-era highs, and natural gas prices remain near eight-year highs. Through September 30, the Bloomberg Commodity Index is up 30% for the calendar year. [7]

Corporate earnings tell a similar story. Higher labor and raw-materials costs are exerting upward pressure on prices as supply-chain disruptions will likely remain widespread well into 2022. Based on second quarter transcripts, “inflation” was mentioned by 44% of companies on earnings conference calls, the most since 2010.[8]

In a quintessential sign of the times, Dollar Tree recently announced it would begin selling items for more than $1 in its Dollar Tree Plus and Dollar Tree stores. Some goods may be listed for as much as $5. [9]

Financial Market Review

After a torrid first half of 2021, the stock market finally cooled off in the third quarter, with the S&P 500 Index up +0.60%. Financial Services posted the largest sector return, gaining 2.7%. Industrials and Materials lagged, posting -4.1% and -3.5% returns, respectively. International stocks were generally negative in Q3 2021, with developed markets down about 1% and emerging markets generating returns in the -8% range. [10]

After a resurgence versus large growth stocks in the first quarter, large value stocks have underperformed growth shares since April. Year to date, large value and large growth shares are up about 15% and 16%, respectively. In mid- and small-company shares, the disparity is far more pronounced. Mid- and small-cap value stocks are up about 18% and 22% in 2021, while mid- and small-cap growth stocks are only up about 9% and 3%. [11]

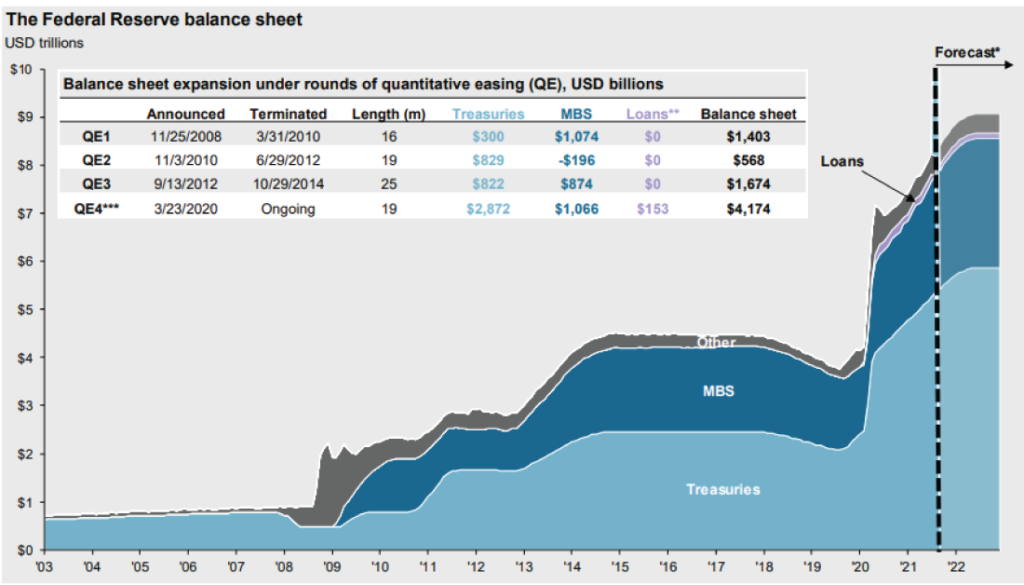

The numerous signals of higher-than- and longer-than-anticipated inflation have precipitated a marked change in the Federal Reserve’s tone. In its September 22 statement, the Fed signaled it will start reducing its $120 billion of monthly purchases in Q4 and will conclude the “taper” by mid-2022. Not only is the tapering faster than expected, but the Fed’s “dot plot” is now signaling a 0.25% rise in short-term rates in 2022, with another 0.75% in both 2023 and 2024. [12] That would still leave short-term rates only around 2.0%.

Source: JP Morgan Guide to the Markets.[13]

Rising yields in the wake of the Fed meeting have weighed on investment grade bond prices. The Barclays Aggregate Index returned -0.9% in September, bringing its year-to-date return down to -1.6%. In contrast, riskier bonds have fared rather well, with high yield “junk” bonds up 4.7% year to date, while syndicated bank loans are up 4.4%. [14]

Market Outlook

Inasmuch as the initial COVID-related shutdowns caused the swiftest bear market in history last March, the subsequent tsunami of federal relief efforts and money supply growth have been a massive boon to stockholders and homeowners alike. U.S. corporate profit margins swelled to an all all-time high in the first quarter of 2021[15], while residential real estate prices are now up 20% versus year-ago levels.[16]

For the past 18 months, asset holders have been enjoying a “free lunch” of higher prices with seemingly few ill effects elsewhere. But as prices for necessities—including rents, fuel, and groceries—have recently spiked[17], it has become increasingly obvious that consumers are starting to feel the squeeze.

As higher inflation eats into the value of interest payments, bondholders are likewise paying the price. And while bourgeoning inflation is finally beginning to eat into corporate profit margins, the next 3-5 years still look a lot better for stockholders than those receiving fixed interest payments.

As science fiction author, Robert Heinlein, and economist, Milton Friedman, both reminded us, “There’s no such thing as a free lunch.” When we compare savings account yields, bond yields, and consumer prices with stock and real estate prices, it’s very clear who’s being served the bigger portions of wealth and who’s been footing most of the bill.

If you have any thoughts or questions regarding capital market conditions and/or financial planning, please contact me.

Disclosures: This material is for informational purposes only and is not rendering or offering to render personalized investment advice or financial planning. This is neither a solicitation nor a recommendation to purchase or sell an investment and should not be relied upon as such. Before taking any action, you should always seek the assistance of a professional who knows your particular situation for advice on taxes, your investments, the law or any other matters that affect you or your business. Although Lighthouse Wealth has made every reasonable effort to ensure that the information provided is accurate, Lighthouse Wealth makes no warranties, expressed or implied, on the information provided. The reader assumes all responsibility for the use of such information.

[1] www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20210922.pdf

[2] ibid

[3] www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20210616.pdf

[4] www.marketwatch.com/story/surge-in-u-s-consumer-prices-slows-in-august-cpi-shows-11631623600

[5] www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20210922.pdf

[7] YCharts. Retrieved October 11, 2021.

[8] www.barrons.com/articles/fedex-results-highlight-inflations-blow-to-earnings-51632496788

[9] www.businessinsider.com/dollar-store-officially-dead-dollar-tree-dollar-general-2021-9

[10] YCharts. Retrieved October 11, 2021.

[11] Ibid

[12] www.reuters.com/business/finance/fed-likely-open-bond-buying-taper-door-hedge-outlook-2021-09-22/

[13] am.jpmorgan.com/us/en/asset-management/adv/insights/markLighthouse Wealth Outlook – October 2021 – WEBet-insights/guide-to-the-markets/. Retrieved October 8, 2021.

[14] YCharts. Retrieved October 11, 2021.

[15] www.cnbc.com/2021/07/23/earnings-season-has-been-great-so-far-with-profit-margins-holding-up-in-the-face-of-inflation.html

[16] www.prnewswire.com/news-releases/sp-corelogic-case-shiller-index-reports-record-high-19-7-annual-home-price-gain-in-july-301386852.html

[17] www.businessinsider.com/rent-prices-increasing-us-cities-zumper-data-2021-9