Download a PDF copy of the Lighthouse Wealth Outlook here: Lighthouse Wealth Outlook – April 2022

Is the Bond Market Warning Us?

Since the inception of the Lighthouse Wealth Outlook, we have warned of the bond market:

January 2021: “Absent a major shift in government policy, most bondholders are virtually guaranteed to lose purchasing power over the next decade. At these rates, even a small increase in yields causes a steep decrease in bond prices.”[1]

July 2021: “At present valuations, we would strongly caution against adding longer-maturity bonds or bonds with elevated credit risk.”[2]

October 2021: “As higher inflation eats into the value of interest payments; bondholders are likewise paying the price. And while bourgeoning inflation is finally beginning to eat into corporate profit margins, the next 3-5 years still look a lot better for stockholders than those receiving fixed interest payments.”[3]

January 2022: “For income-minded investors, we would generally encourage holding some combination of low-volatility REIT’s, short-duration mortgage bond funds and cash in lieu of longer-duration bonds.”[4]

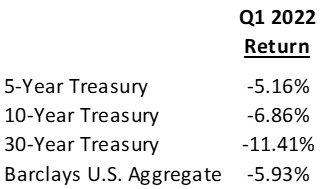

Unfortunately, those projections have proven correct. Since we penned that last statement earlier this year, bonds have undergone their most severe correction in at least four decades.

Source: am.jpmorgan.com/us/en/asset-management/protected/adv/insights/market-insights/guide-to-the-markets/. Retrieved April 10, 2022.

Though we do not enjoy having accurately predicted this collapse within the bond market, we were able to project it by evaluating then-current economic conditions, largely caused by the pandemic, through the lens of two bond basics:

- Inflation is very bad for returns.

- The lower the yield, the riskier the price

Flattening The (Healthcare) Curve

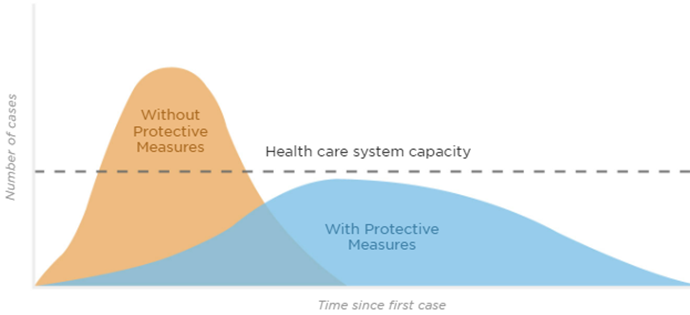

When COVID-19 first landed in the United States, various stay-at-home mandates were put in place to “flatten the curve.” The initial intent of mandated lockdowns was to reduce the short-term stress on the healthcare system.

Source: am.jpmorgan.com/us/en/asset-management/protected/adv/insights/market-insights/guide-to-the-markets/. Retrieved April 10, 2022.

The consequent decline in economic activity was staggering, with GDP dropping by nearly one-third in the second quarter of 2020. But with the timely injection of trillions of government stimulus, U.S. output quickly snapped back, making the two-month COVID recession the shortest recession in American history.[5]

In many respects, the federal response to COVID-19 paralleled its response to the Global Financial Crisis a dozen years ago. However, there were several meaningful differences in the magnitude of the various relief measures:

Source: www.cbo.gov/sites/default/files/cbofiles/attachments/02-22-ARRA.pdf, Ycharts.com

As the Coronavirus Aid, Relief and Economic Security (CARES) Act landed directly in consumer and business bank accounts, the Federal Reserve bought nearly all of the new Treasury borrowing needed to fund the programs. Accordingly, the money supply swelled by nearly 40% in less than two years.[6]

While the massive increase in the money supply was setting the stage for widespread inflation, bond yields were absolutely paltry. The yield on the 10-year U.S. Treasury note hit a record closing low at 0.501% during March 2020. By the end of the year, it was still only 0.93%. By New Year’s Eve 2021, the 10-year was still only paying 1.52%.[7]

To reiterate: by correctly anticipating high inflation due to the new money creation and observing that U.S. bond yields were near all-time lows, we were able to forecast a dire outlook for bonds that has since materialized.

So, what’s next?

Flattening The (Yield) Curve

On the morning of Tuesday, April 12th, the U.S. Bureau of Labor Statistics reported that the Consumer Price Index (CPI) rose by 8.5% year-over-year in March 2022. It marked the 22nd consecutive monthly increase in CPI and the highest CPI print since 1981. “Core inflation,” which omits food and energy prices, rose 6.5% on the year, the highest rate since 1991.[8]

At the same time that inflation has been rising, unemployment has been collapsing. In its most recent release, the Labor Department reported that the national unemployment rate is 3.6%, barely above the 50-year low of 3.5% it registered just before the pandemic.[9] Average hourly earnings were also up 5.6% from a year ago.[10]

Rising inflation amidst falling unemployment is (finally!) forcing the Federal Reserve to raise short-term interest rates in a bid to stem price increases. In its March meeting, the Fed raised interest rates by 0.25%, the first in what is now expected to be several increases this year. Its most recent “dot-plot” is now forecasting a target short-term rate of 1.9% by the end of 2022.[11]

The Fed is also concluding its 29-month asset purchase program, also known as “Quantitative Easing,” and is expected to actually decrease its balance sheet in the next several months.[12]

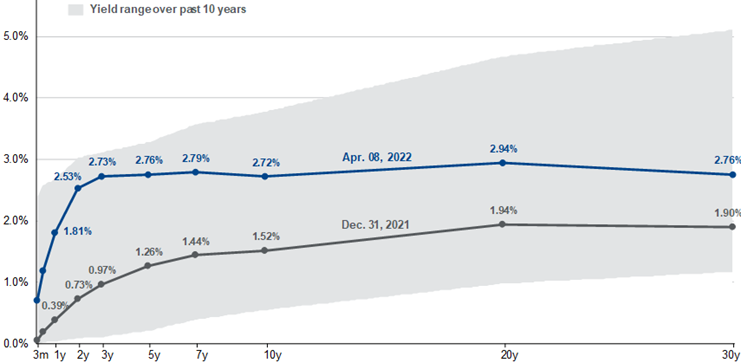

While bond yields of all maturities have risen markedly since January 1st, expectations of a more aggressive Fed have caused short-term rates to climb faster than long-term rates. This dynamic is known as a “flattening yield curve.” The graph below contrasts the U.S. Treasury yield curve on two dates: December 31, 2021, and April 8, 2022.

Source: am.jpmorgan.com/us/en/asset-management/protected/adv/insights/market-insights/guide-to-the-markets/. Retrieved April 10, 2022

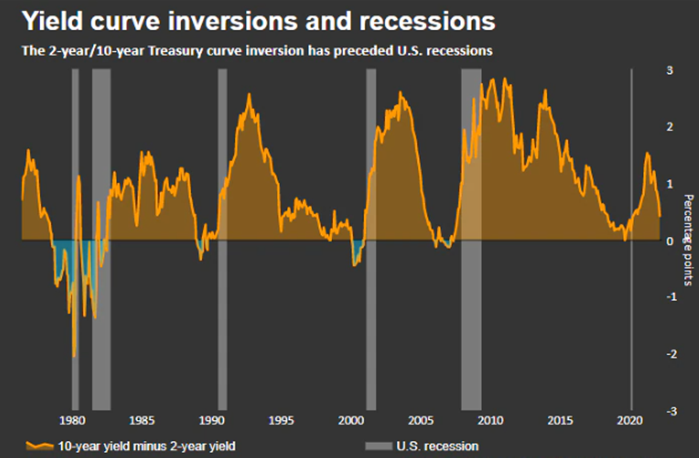

On March 31st, the two-year yield briefly surpassed the 10-year yield. The technical implication: beginning at least two years from now, short-term interest rates will be reduced. The economic implication: a recession is coming in the next six to 24 months.[13]

A well-recognized recession indicator, the 2s/10s curve has inverted before each recession since 1955, with a recession following between six and 24 months. It offered only one false signal in that timeframe. The last time 2/10s inverted was in 2019—just before the 2020 pandemic recession.[14]

Source: www.reuters.com/business/finance/us-yield-curve-inversion-what-is-it-telling-us-2022-03-29/

Economic Conditions

In addition to the inverted yield curve, there are several other reasons to anticipate a recession within the next year or two:

- Gas prices are above $4 a gallon, hitting consumers hard in the wallet.[15]

- Food prices are likewise weighing on household budgets. Russia is the world’s number one wheat exporter; Ukraine is number three. Their conflict has the U.N. Food and Agriculture Organization (FAO) projecting that international food and feed prices will rise by 8-22% from their already elevated levels.[16]

- Fertilizer is about three to four times costlier now than in 2020, also due to the Russia-Ukraine turmoil. This also heralds higher food prices.[17]

- 30-year mortgage rates are hovering around 5%, their highest rate since 2018. Monthly payments have risen by 28% from year-ago levels.[18]

- The Federal Reserve is forecasting real GDP growth of 2.8% in 2022, down from a 4.0% prediction in December.[19]

However, several positive items may reduce the severity of a downturn:

- Though still much flatter than three months ago, the 2s/10s curve is no longer inverted.[20]

- S. household net worth surged almost $19 trillion in 2021.[21] As consumers have been saving and paying down debt for two years, their balance sheets are in good shape.

- Despite a large run-up, real estate values still look reasonable relative to rental rates. (That was not the case in 2007!) At the current sales pace, the supply of homes on the market would last only 1.7 months.[22]

- The U.S. dollar has risen over 10% in less than a year, making U.S. imports less expensive.[23]

Financial Market Review and Outlook

In addition to pummeling bond prices, rising interest rates and Russia-Ukraine headlines categorically weighed on stocks in the first quarter. After dropping below 12% through March 14, the S&P 500 rebounded sharply to finish the first quarter at -4.6%. International shares slumped by 6-7%.[24]

In contrast, commodity prices spiked on supply shortages. The Bloomberg Commodity Index climbed 25% in the first quarter as petroleum, grain and gold prices all climbed.[25]

While we believe that a recession in the next two years is a very strong probability, we are still disinclined to shift allocations from stocks to bonds for at least two reasons:

- Corporate earnings generally increase with inflation as companies pass through many of their rising costs onto customers. In contrast, most bond payments are static.

- While bond yields are markedly higher than on December 31st, they are still very low by historical standards and still carry a fair amount of downside risk. Stocks remain comparatively cheap versus bonds.

Disclosures: This material is for informational purposes only and is not rendering or offering to render personalized investment advice or financial planning. This is neither a solicitation nor a recommendation to purchase or sell an investment and should not be relied upon as such. Before taking any action, you should always seek the assistance of a professional who knows your particular situation for advice on taxes, your investments, the law or any other matters that affect you or your business. Although Lighthouse Wealth has made every reasonable effort to ensure that the information provided is accurate, Lighthouse Wealth makes no warranties, expressed or implied, on the information provided. The reader assumes all responsibility for the use of such information.

[1] www.bssfwealth.com/blog/january-2021-outlook

[2] www.bssfwealth.com/blog/outlook-july-2021

[3] bssfwealth.com/blog/lighthouse-wealth-outlook-october-2021

[4] bssfwealth.com/blog/lighthouse-wealth-outlook-january-2022

[5] cnbc.com/2021/07/19/its-official-the-covid-recession-lasted-just-two-months-the-shortest-in-us-history.html

[6] Ycharts.com

[7] ibid

[8] www.thestreet.com/markets/inflation-soars-to-new-40-year-high-in-march-core-pressures-ease

[9] www.wsj.com/articles/how-low-can-unemployment-go-11648826445

[10] www.barrons.com/articles/jobs-hiring-inflation-wages-51648847543

[11] www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20220316.pdf

[12] ibid

[13] Ycharts.com

[14] www.reuters.com/business/finance/us-yield-curve-inversion-what-is-it-telling-us-2022-03-29/

[15] Ycharts.com

[16] www.fao.org/3/cb9013en/cb9013en.pdf

[17] www.wsj.com/articles/fertilizer-prices-surge-as-ukraine-war-cuts-supply-leaving-farmers-shocked-11648114381

[18] www.nar.realtor/newsroom/existing-home-sales-fade-7-2-in-february

[19] www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20220316.pdf

[20] ibid

[21] awealthofcommonsense.com/2022/03/how-to-prepare-for-a-recession

[22] www.nar.realtor/newsroom/existing-home-sales-fade-7-2-in-february

[23] YCharts

[24] ibid

[25] ibid